Exceptional Items After Tax Calculation

Exceptional Items after tax are calculated as follow:

Exceptional items AT = Exceptional Items - Tax on Exceptional Items

Tax on Exceptional items = (Tax * exceptional items)/ PBT

Notes:

- If the tax of exceptional income is more than the exceptional item itself, then the Exceptional item AT will be equal to the Exceptional item

- Profit / loss on sale of fixed assets is always classified as exceptional item to keep it same across all companies. [This is not adjusted for post-tax].

- Profit from associates is always classified under "other ordinary income"

- Profit from sale of associate (or investments in associate) is classified under "exceptional items"

Examples

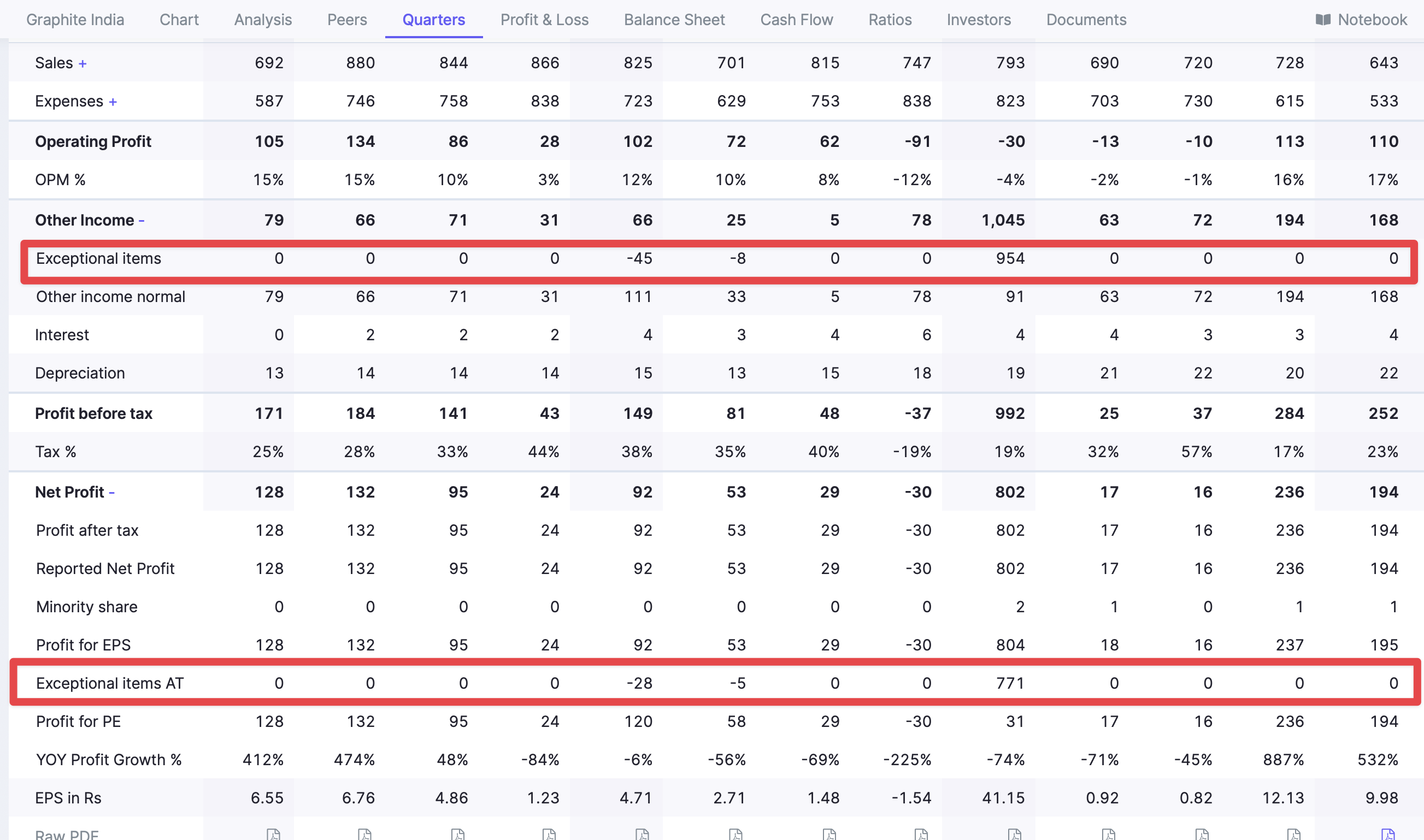

Let's take the example of Graphite India, where the company sold its land in Mumbai and made 954 Crs as exceptional income

Tax = 188.5 Crs

Exceptional items = 954 Crs

PBT= 992 Crs

Tax on Exceptional items = (188.5* 954)/992 = 181 Crs

Exceptional Items AT = 954 Crs - 181 Crs = 773 Crs

Tata Motors - March 2024

Canara Bank - Mar 2024

Exceptional Items = 16.31 Cr

Tax = 5217 Cr

PBT = 19,999

=> Tax on exceptional = 5217 /19999 * 16.31 = 4.17

=> Exceptional after tax = 16-4.17

Issue 1:

When the exceptional item is negative and when the tax% is also negative. Ex: Tata Motors March 24 Qtr

When the exceptional item is relatively small compoared to PBT. Ex: Canara Bank FY24